Latest Articles

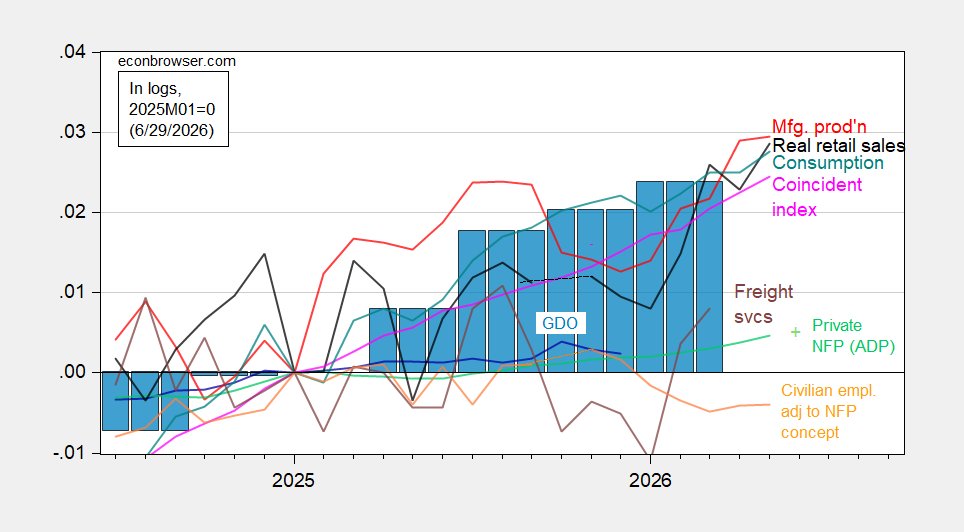

Alternative Business Cycle Indicators: Coincident, Consensus ADP

0

2

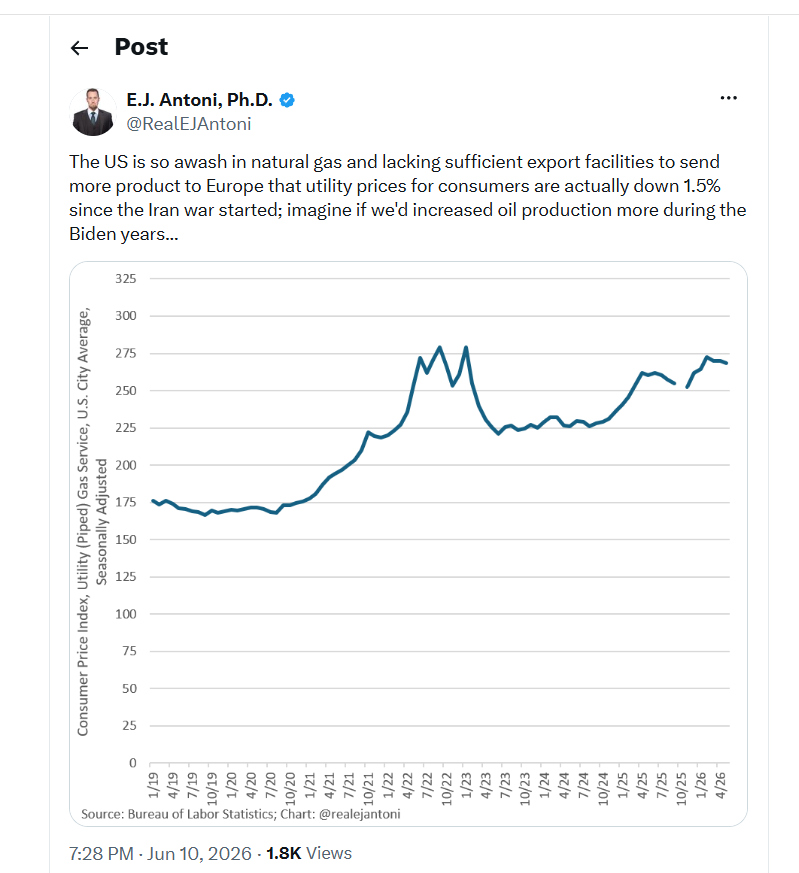

EJ Antoni: “E.J. Antoni: U.S. utility prices down 1.5% since Iran war began”

0

2

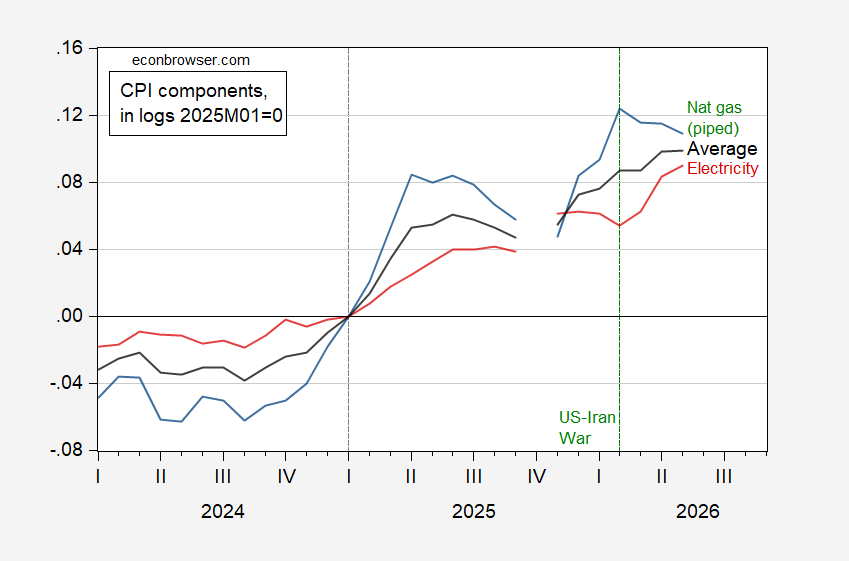

Imagining: Would a Biden “Drill, Baby, Drill” Regime Have Mitigated a Iran-War Induced Cost-Push Shock

0

1

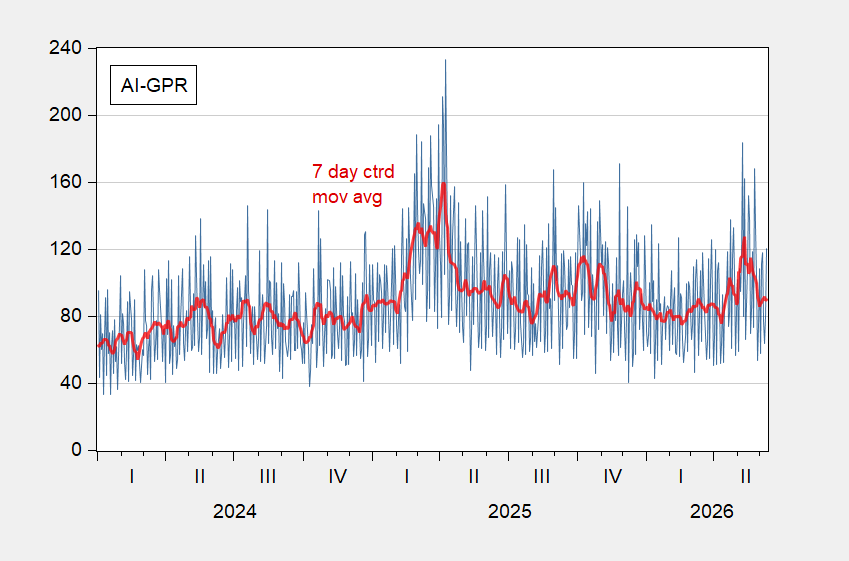

Invaluable New Geopolitical Risk Indexes: AI-GPR, GPR-Oil, and More

0

1

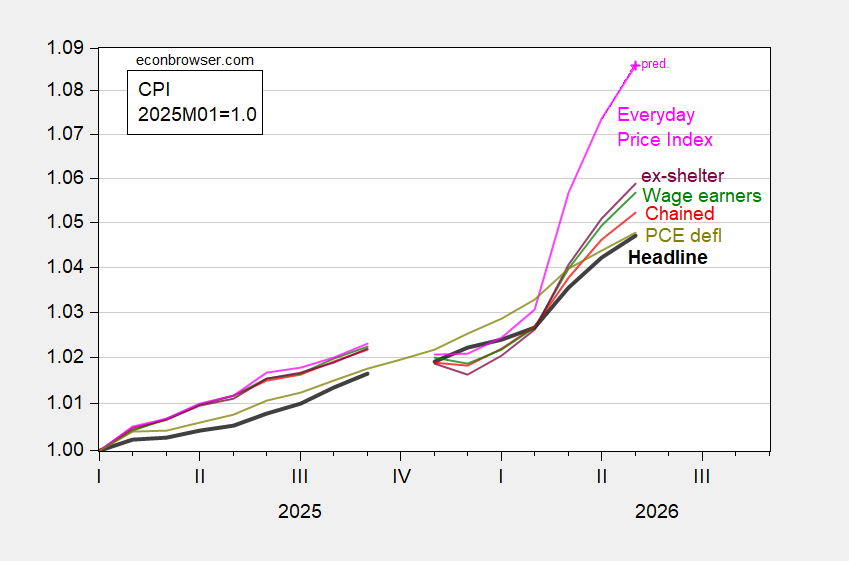

Headline CPI Inflation at Consensus, Real Wages Continue to Be Eroded

0

1